Mortgage Changes in 2023

The last half of 2022 was a difficult year for the mortgage industry and here come mortgage changes in 2023. The massive drop in the volume of mortgages (down perhaps 80% or more from the year earlier) caused many, many layoffs, bankruptcies and closures of mortgage companies in late 2022. Cheap, easy money disappeared. Where buyers essentially faced auctions to pay the highest price for a house in 2021 and early 2022, the market cratered in the last half of 2022 with rampant price cutting. Affordability has been an issue for the last two years, whether from overpaying to buy in 2021 or rate increases in 2022. Prepare for the coming opportunity with Winning Mortgage, Winning Home.

Just in- FHA cuts the Mortgage Insurance Premium by 30 basis points. What does that mean? If you are a poor credit risk with minimal down payment and as a borrower are 3.5x as likely to default as a conventional borrower, politicians are going to risk more taxpayer money to help you buy a house.

Home Sales Cratered

According to the Realtor’s trade group, sales of existing homes have now fallen for 11 straight months ending December 2022. December saw the slowest sales rate since 2010—the trough of the financial crisis. Mortgage rates have fallen a full percentage point since their October 2022 peak. But they remain about double what they were one year ago. Softness in sales will continue until the Fed ends interest rate increases somewhere around mid 2023.

“Markets in roughly half of the country are likely to offer potential buyers discounted prices compared to last year,” added the NAR. Homes are sitting on the market longer. Lack of buyers ended the strong sellers market of 2020-2021. While sales are down in all price categories, they are falling most sharply on the higher end. Sales of homes priced above $1 million were down 45% year over year, compared with sales of homes priced between $250,000 and $500,000, which were down 34%.

Changes for 2023

For 2023, the maximum amount allowed for a conforming mortgage jumps substantially. While existing owners have equity in their homes, cash-out refinancing is getting harder and more expensive. Those who bought in late 2020 to early 2022 think they have a lot of equity in their homes. But substantial price drops across much of the country show that this equity may be illusory.

Under new rules, cash-out refinancing will be more expensive and harder to get in 2023. And thanks go to the government agency controlling Freddie Mac and Fannie Mae. In October, the Federal Housing Finance Agency (FHFA) announced it will implement targeted increases to the upfront fees for most cash-out refinance loans. The implementation, begins February 1, 2023. As a result, Freddie Mac said in December that when proceeds of a cash-out refinance are used to pay off a first lien mortgage, it must be seasoned for at least 12 months. A borrower has to wait 12 months to get new cash out after buying a house, getting a rate-and-term, or getting a cash-out refi. Fannie Mae will likely follow Freddie Mac with the changes.

Loan Limits for Conventional Mortgages Rise

In 2023, borrowers will be able to get larger loan amounts in conforming loans. The limit rises from $647,200 to $726,200 in most areas. However, it also rises from $970,800 to $1,089,300 in high cost areas. Both Fannie Mae and Freddie Mac use these limits. Loan amounts greater than these limits are considered “Jumbo Loans.” Under the charters for Fannie Mae and Freddie Mac, they are supposed to be organized to provide loans for affordable housing. So $1 million is now affordable??? Investor loans for multiple unit properties also rise.

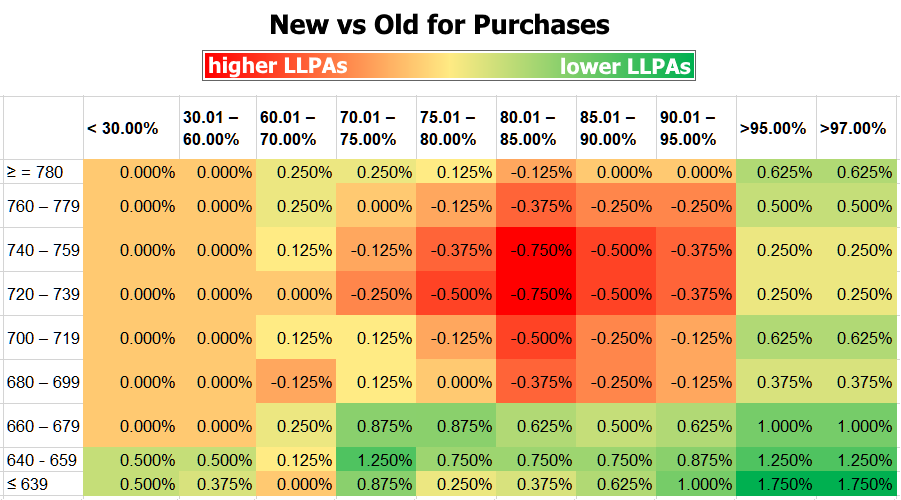

LLPAs Change May 1, 2023

The effective penalty for having a credit score under 680 is now smaller than it was. So closing costs for low credit fall, but rise for other borrowers. Read Winning Mortgage, Winning Home to understand LLPAs and how they affect you. Borrowers with higher credit scores will generally be paying a bit more than they were under the previous structure. The following chart shows the differences. Green and yellow cells show where things have become more affordable than they were. Orange and red cells = more expensive. These changes are POLITICAL. Higher risk borrowers/low income borrowers had risk adjusted fees lowered while frugal, money managing, lower risk borrowers had fees increased. These changes don’t make sense. However, borrowers who are refinancing and taking cash out will pay higher fees than a straight loan without taking cash out. At least this one change makes sense.

Other Mortgage Changes

There are many other changes. A new charge for DEBT-TO-INCOME (DTI) ratio. Higher DTI ratio borrowers borrowing more than 60% will pay more. Most borrowers for home purchase are borrowing 80%-95%, so this affects most borrowers with a total DTI over 40%. If you try to borrow what you qualify for, this will be you!!! You will need to borrow less than you qualify for to avoid these charges.

A few other examples of changes:

- There are new credit score bands at 760+ and 780+.

- BIG increases in fees for many “Cash-Out” loans

FHA Delinquencies (30 days past due) have nearly doubled from April 2022 to December 2022.

The fate of Federal Housing Administration (FHA)-backed mortgages in the ongoing downcycle housing market may be the canary in the coal mine of mortgage distress. In recent months, this canary has been chirping in the face of inflation, rising mortgage rates, declining home values, and the potential of faster-rising unemployment. All this spurs fear of a potential recession in the coming year. First-time homebuyers represent more than 80% of FHA’s loan volume each year. This means that first time homebuyers may not have completely understood the risk they were taking by FOMO bidding for houses.

Over the past 14 years, FHA has insured 9.1 million in mortgages valued at $1.7 trillion to first-time homebuyers. In addition, FHA insured about 75% of all high loan-to-value (LTV) mortgages made to first-time homebuyers with credit scores below 680. More than 25% of FHA-insured purchase-mortgage holders with loans originated during the first nine months of 2022 have dipped into negative equity, according to a recent Black Knight report, and nearly three-quarters have less than 10% equity in their properties.

As a result, the FHA could be facing a wave of future defaults, depending on the severity of home-value declines over the next year, the pace of inflation and the potential for rising unemployment if the economy moves toward a recession on the heels of the Federal Reserve’s monetary tightening policy.

Seller Concessions and Rate Buydowns

Sellers are attracting buyers to their homes through temporary mortgage rate buydowns. A seller escrows a portion of the purchase price as a give-back/concession to the buyer. The money goes into an escrow account to temporarily lower the interest rate for a period of 1-2 years. Buyers gamble that mortgage interest rates will fall over the next 1-2 years from the initial rate. Then the buyer refinances to the new, longer term, lower rate. Any unused escrowed money goes toward the lowering the loan balance at the time of refinancing. If rates don’t fall or rise, the buyer is stuck with the initial rate. However, look for more mortgage changes in 2023 as rates see saw and the Federal Reserve continues battling inflation and recession.

According to a new Redfin report, a record 41.9% of home sellers gave concessions to homebuyers in the fourth quarter of 2022 through money for repairs and mortgage-rate buydowns.

Lower Rents?

For the two years from mid-2020 to mid-2022 homes prices rose quickly. This meant the values of rental houses also increases. The higher prices paid resulted in higher property taxes and property insurance costs not just for buyers, but for existing home owners. Following that, renters faced large rent increases based on the higher prices paid, higher property taxes, and higher property insurance costs for investment properties. But home price appreciation stopped dead in mid 2022. Homes have been decreasing in price every month since. Concessions by sellers, rare in 2021 and early 2022 have now hit 41% of sales coupled with drops in asking prices. Declining rents are highly likely in 2023. The first hints of the downturn showed up at the end of the 3rd quarter of 2022. That was three months after sales prices started declining. Apartments saw very weak demand.

It’s gotten steadily worse since then. According to Apartment List, rents fell nationally every month in the fourth quarter. Rents fell nationally by an average of 0.9% each month in the fourth quarter. New lease demand cratered in the second half of the year, and was negative for the full year for the first time since 2009.

The national apartment vacancy rate rose to 5.9% in December, its highest level since April 2021. Vacancies are noted as still rising by 0.2% per month. And there are more apartment units under construction than there have been in more than 50 years. More supply equals more vacancy equals more competition for tenants equals even lower rents or more concessions. And on top of that are forecasts of increasing job losses.

So what?

Add it all up and the market is likely to continue to soften. Home buyers will see more advantages as 2023 progresses.