A Foreclosure Crisis?

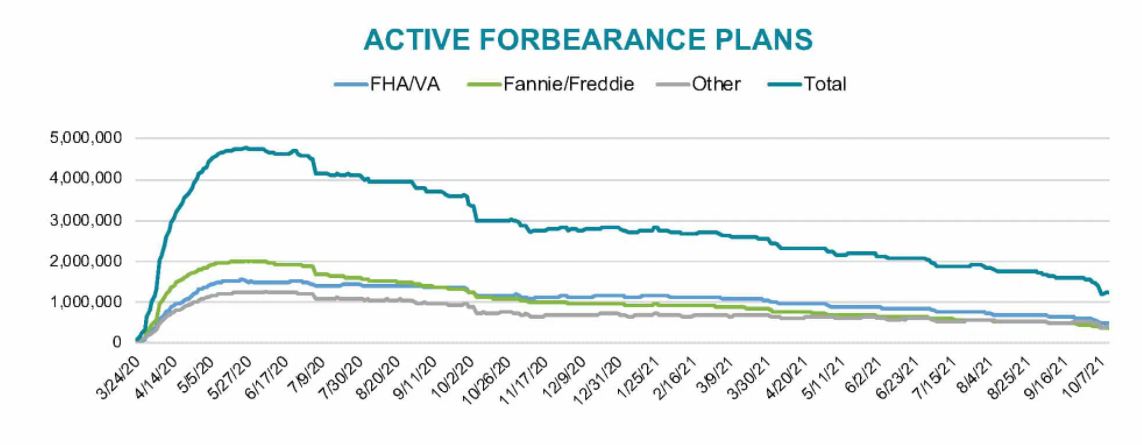

Is it possible that a foreclosure crisis is brewing? In prior posts we noted that forbearance was extended to June 30, 2021. Reports showed that more than 5% of mortgages remained in forbearance after a year. That number recently fell to about 2.5 million still in forbearance as workouts and exits progressed. New entrants into forbearance declined significantly in late 2020 and early 2021. Many who entered forbearance entered a modification or caught up on mortgage payments. This represents a primary reason the number of loans in forbearance dropped. A low number of new entrants coupled with the high number of loans still in forbearance indicates potential trouble. Perhaps a large majority of those 2.5 million loans still in forbearance have little or no expectation of emerging from forbearance except though a default. Will the number who fail to resume payments be manageable or will it disrupt the market?

While a morbid fact, 700,000 deaths in the US from Covid have been recorded. Many of these are elderly in long term care facilities and without homes/mortgages. But effects have been broad. The reality is that death has an impact on ability of many to repay loans. Income lost and needed to support mortgage debt may make debt unmanageable without life insurance.

Loans in Forbearance Still an Issue

Over half of delinquent homeowners have missed six payments. CoreLogic, a major housing information company, estimates that about one million homeowners have not made a monthly mortgage payment in more than a year. The national delinquency rate, the percentage of home mortgages that were 30 or more days past due in July, including those in foreclosure, was 4.2 percent.

Most recently in October, 1.25 million loans remained in COVID-19 related plans. This represents 2.4 percent of the nation’s 53 million active mortgages. The breakdown is 376,000 GSE (Fannie Mae/Freddie Mac) loans, 1.3 percent of those totals. 485,000 FHA and VA loans (4.0 percent) and 386,000 portfolio/PLS loans (3.0) also remained. The loans have a combined unpaid principal balance of $233 billion. As was probably inevitable, foreclosure files rose significantly in the third quarter of 2021. They accelerated in September. The moratorium on foreclosures which was put in place in March 2020 in response to the COVID-19 pandemic expired on July 31.

Now that the forbearance and Covid actions have expired, what can delinquent borrowers expect? If income has not returned to a level to support the loan, borrowers need to face reality. Foreclosure may be imminent. That has not been the case so far. A data firm found that nearly a third of borrowers who start the foreclosure process with at least 40% equity in their homes go to foreclosure anyway. That means the borrower loses unless the borrower sells. A borrower may not be able to buy another home immediately since income hasn’t returned. But financial reality means selling, pocketing the money, and renting for a period of time. Why let 40% of the value of your home vanish?

Foreclosure Activity

ATTOM (a housing information company), in its Q3 2021 U.S. Foreclosure Market Report says there were 45,517 foreclosure filings. It was the first quarter-over-quarter double digit increase since 2014. Nationwide one in every 3,019 properties had a foreclosure filing during the third quarter. The highest incidence was in Nevada, one of the states that consistently was at the top of filings throughout the 2007-2011 foreclosure crisis. During the third quarter one in 1,463 Nevada properties received a filing. Illinois was second (one in every 1,465 properties), followed by Delaware (one in every 1,515); New Jersey (one in every 1,667); and Florida (one in every 1,743). Among the 220 metropolitan statistical areas that ATTOM tracks, the highest filing rates were in were Atlantic City, Peoria, Bakersfield, Cleveland, and Las Vegas.

The Foreclosure Market

Foreclosures won’t happen all at once when forbearance ends. Some individuals entering late into forbearance may remain there until 2022. However, a majority of loans in forbearance have a deadline of September 30, 2021. The volume of possible foreclosures will build towards Q3/Q4 2021 as noted in our window for an advantageous purchase. Looking at the number of mortgages that are delinquent and in forbearance, a foreclosure crisis seems unlikely. However, many expect a minimum of 500,000 to 700,000 foreclosures in process or completed by Q4 2021 into 2022 from those currently in forbearance. The most recent numbers show a large recent jump in foreclosure postings. The CFPB and FHFA also have plans under consideration to slow foreclosures. Which only means delay, not prevent.

Where Delinquencies are Focused

Where might this foreclosure wave start? The process already started, but it takes at least 120 to 180 days. Foreclosure filing increases point to early 2022 for the actual foreclosure wave to pick up steam. Recent data shows New Jersey with highest FHA delinquency rate at about 20%. Nevada, New York, Florida, and Hawaii closely follow New Jersey. Loans in forbearance CANNOT be reported as delinquent. Forbearance masks the actual number of loans in distress. In addition to loans in forbearance, many mortgage loans have become delinquent but weren’t eligible for forbearance. Note that only federally backed loans (about 70% of mortgages) require lenders to permit forbearance. The other 30% of mortgages lack the protection of forbearance. Delinquent loans (not in forbearance) need to be considered as part of the potential number of foreclosures. This chart notes those additional delinquencies. This may indicate where a foreclosure crisis is brewing.

The biggest issue driving increases in pricing today is FOMO, lack of supply and massive spikes in prices of building materials. Lumber prices quintupled in early 2021 but have since come down. This added $35,000 to $45,000 to the cost of a new house. Builders delayed starting new homes for months.

On the re-sale side, large numbers of borrowers refinanced. That may mean the amount of existing homes for sale may fall from prior years as borrowers stay in a house longer.